TGIF...

—'ing Over!

First published in our weekly newsletter on October 5, 2024.

Yes, last week’s drying paint was due to the JPM Call

...and yes, it was entirely foreseeable

Devilish timing, of course- but the fact is, this was entirely foreseeable.

...and it just goes to show how absolutely critical it is that you KNOW the flows- and positions.

While many traders enthusiastically geared up for the well telegraphed “Window of Weakness” expected to hit alongside bearish late Sep seasonality in the index- the market had tricks, not treats up its sleeve.

Typically, the index “loosens up” after an AM Opex. This happens because the AM serial still tends to attract the largest concentrations of dealer long gamma vs any other day on the calendar. The reason is probably far less sexy than you think-

Customer selling flows work like this:

Some sellers short vol every day on the calendar

Some sellers only short vol every Monday, Wednesday, and Friday

Some sellers short vol on Fridays only

Some sellers short vol on the 3rd Friday, AM Opex only

End of month is a better mixture of short vol + hedging

Stack all those up on a calendar and what do you have? A pile-up on the Monthly OPEX.

Now, when that expiration comes around... some inventory is rolled, and some of it is taken into the settlement and reset thereafter.

For the crowd that sells 1-month vol, they’re resetting into the next serial expiration. When they do so, they’re replacing that expired option with a ~28dte option.

Since gamma is maximum at expiration- this means that *even if they replaced every contract 1 for 1*, the gamma drop is immense... and those new positions don’t contribute much long gamma for the dealer community *until* they are near expiration again, the following month.

The Window of Weakness concept

arises out of the assumptions around the traditional dealer profile- and the inventory you’d *assume* would be expiring during Opex week.

Now of course not every Opex yields those “supportive charm and vanna flows” we’ve all come to take for granted- that requires long-calls above, and short-puts below. But the generalization has stuck around and become entrenched in the vol-tourist community.

Sep Opex was supposed to bring violence

thanks to the additional layer of the well-telegraphed seasonal weakness which was to be expected into late Sep & early Oct. Instead...

WELCOME TO THE UNCLENCHING

Instead, we got PINNED.

And there was NO EXCUSE to be surprised by this one.

Regardless of any assumptions around the positions rolling off during Sep OPEX, it was obvious once we closed around 5700 that the massive concentration of dealer long calls around 5750 in Sep Quarterly... just 6 trading days out... would be all but impossible to escape.

I won’t go into all the details here (because that’s what tomorrow’s call is for) but I DO want to take a moment, and “put a number on it”... so you get a feel for just how strong of an influence a position like this creates.

Remember... dealers need to stay delta-neutral.

In practice, this means they’ll buy or sell ES futures depending on how their position’s total delta changes. If they get short delta- they buy futures to get back to flat. If they get long delta- they sell futures to get back to flat.

Simple.

Well- we knew the position (long ~39.6k SepQ 5750 Calls).

All you need to do from there is understand the flows. That’s what I’m here for 🍻

Gamma Slows, while Charm Traps

Approaching 5750 from below, dealers were getting longer and longer gamma.

Let’s walk through that-

Remember- dealers want to stay delta neutral.

Long Gamma =

if SPX UP, dealers get long delta = dealers must SELL futures

if SPX DOWN, dealers get short delta = dealers must BUY futures

“..dealers were getting longer and longer gamma.”

This means as we approached 5750, the strength of that influence was GROWING.

This SLOWS the market as the market approaches the strike level- because with every dollar higher, dealers have to sell an even GREATER number of futures to get their delta back to flat.

It then compresses the price action around the strike- as the long gamma requires dealers to be buying futures on downticks as well.

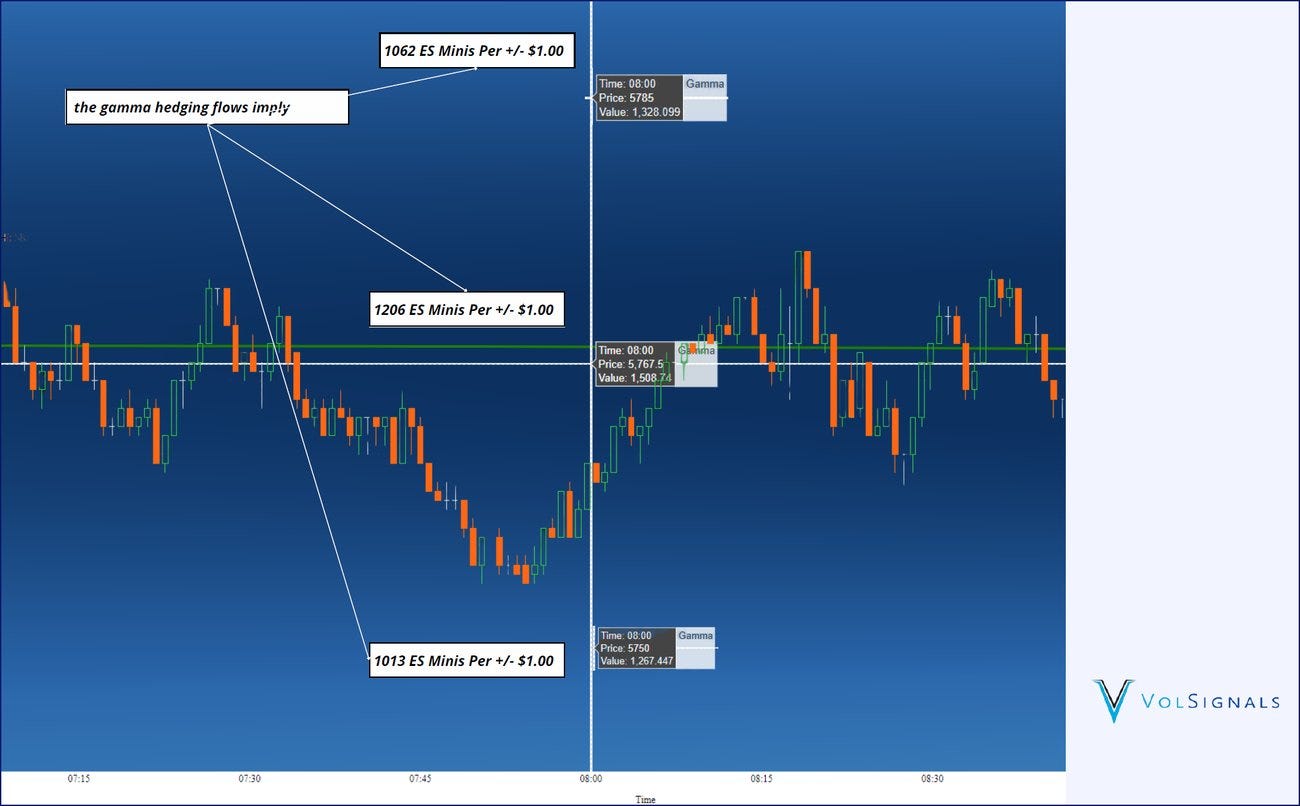

Just how big was this influence last week?

For most of last week, dealers would have to buy ~1k futures or more FOR EVERY DOLLAR the market dropped (or sell ~1k futures or more FOR EVERY DOLLAR the market rallied).

See why it gets so sticky?

Take a look at the implied gamma flows on Thursday morning, from our premarket call:

and what about Charm?

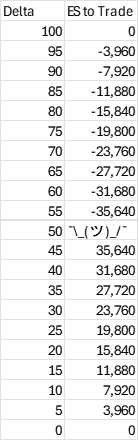

Charm = “delta decay”

For an easy way to wrap your head around it- just ask yourself the question:

“What if this call expired now?”

To answer that question, you’d then check the *current* call delta (left-hand side).

On Friday at the close, the delta was around 35.

<< look across to the right hand side >>

Expiring the call would require dealers to BUY 27,720 FUTURES

Luckily that process is NOT actually instantaneous- it’s gradual and dynamic, changing with time, spot level and implied vol as we approach Monday’s settlement.

That said— it’s this *passive* influence which serves to trap the market on the dealer’s largest strike.

If we’re ABOVE the strike, it’s the opposite. Dealers are passively selling futures until expiration- helping nudge the market towards that ultimate PIN.

This is why I drill these concepts all the time- because these forces are *in play* all the time- just to varying degrees.

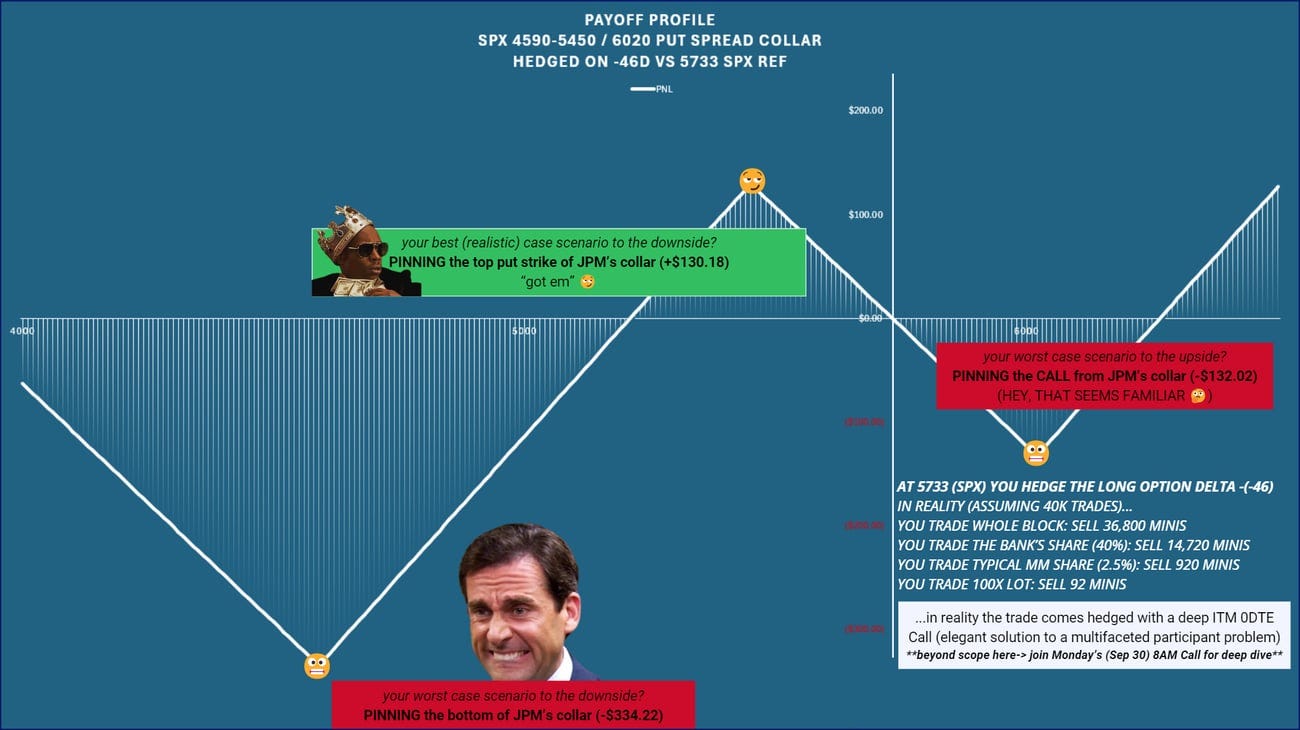

VolStudies: Graphing the Collar’s Expiration PNL

In VolStudies, we’re graphing Expiration PNLs...

Far from trivial- these are the fundamentals which you drill as a trainee with most option market making firms.

You start simple- and then add extra contracts. Longs vs shorts. A hedge asset, etc.-

(For a longer explanation, read through my thread HERE)

Eventually, you do so many that they become second nature.

Name any trade, and instantly/intuitively you should be able to ballpark the breakevens and both best- and worst-case outcomes for the dealer hedging the trade once and holding it until expiration.

Of course in real life you’re hedging dynamically and offsetting your trade with other trades- hopefully AVOIDING position concentrations altogether.

Ultimately, when trades offset one another, the actual position you carry is much easier to manage.

It’s CONCENTRATION that becomes a problem- and that’s why it’s CONCENTRATION that I’m constantly looking for (and talking about) in the market.

Case in point...

...check out that graph above.

Now this particular PNL profile is forward looking. It’s an estimate of the strikes which may trade tomorrow, given an SPX reference of 5733. Depending on volatility levels, the actual call strike could be higher or lower- but the basics are going to be the same.

JPM Call PIN (5750) = MAX PAIN (for the dealer/MM)

That profile is a simplification- but the main points are 1000% accurate.

The dealer’s WORST CASE OUTCOME is landing on the strike at expiry.

I’ll discuss in greater detail just WHY that is on tomorrow’s free call- “TGIF—’ing Over!”

just get on the list and your invite goes out 7:04 AM sharp 🔒

Stay tuned. . .

ahead this week:

Behind the PIN

A look at what lies in wait once SepQ rolls off...

Chat soon 🍻

— VS —